11 May 2009

Hospitality Lawyer Insights from Meet the Money® 2009: If it is available, you want leverage to increase your yield, right? Not so fast, says a new study that may amaze you!

The hospitality lawyers of JMBM’s Global Hospitality Group® have presented an annual hotel conference for 19 years. On May 5-7, 2009 in Los Angeles, California, Meet the Money® 2009 was held at the Sheraton LAX for almost 400 industry leaders.

Presentations from Hotel Industry thought leaders by JMBM’s hospitality lawyers

The PowerPoint presentations from a number of industry leaders at Meet the Money® 2009 are listed with hyperlinks at JEWELS from Meet the Money® 2009 — the “best ever” hotel conference.

Commentary and observations from the hospitality lawyers of JMBM and other industry experts on some of the critical industry issues are available at Hospitality Lawyer Insights.

Here is the first in the Hospitality Lawyer Insights series on some of the most critical issues of our day.

#1. Is leverage dead or just deadly — a controversial new investment reality may be taking hold

We are in a credit crunch, so we expect a dearth of leverage, even if it is painful. The new reality is part of complete “reset” our economy and investment approach must accommodate before we can recover. The extent of this reset may surprise and appall you as revealed by the industry leaders at our recent conference. But John Arabia’s new thesis is even more amazing.

First, the new reality:

Robert B. Stiles:

Robert B. Stiles

Executive Vice President & Principal

Cushman & Wakefield Sonnenblick Goldman

(415) 658-3601

robert.stiles@cushwake.com

“It would have been very difficult to win a deal in the last 5 years if you were not levered.”

Bernard N. Siegel:

Bernard N. Siegel

Principal

KSL Capital Partners, LLC

(720) 284-6440

bernard.siegel@kslcapital.com

“We are seeing some of the best companies, properties, and sponsors under stress. They may not be making debt service. They can’t wait for the industry to turn around because they may not be able to service their debt.

The equity investor demands the highest return on or has the highest cost of capital (high teens, unlevered)…and we have another wave of foreclosures and debt restructuring still ahead. Any deal that closed in ’06, ’07, or ’08 is basically underwater now.”

Bruce G. Wiles:

Bruce G. Wiles

Managing Director & Principal

Thayer Lodging Group

(301) 581-5910

bruce.wiles@meristar.com

“There will be a deleveraging. You have to rework your capital stack.

Debt sizing we see today is 40% for debt, with equity-type yields over that. There is about a 2 to 1 debt coverage. Elements of recourse are creeping into loans, and guarantees by sponsors at least of certain things.”

David Loeb, RW Baird & Co:

David Loeb

Managing Director

RW Baird & Co

414-765-7063

dloeb@rwbaird.com

“Public markets are likely the key to a broader real estate de-levering – $7.2 billion

To de-leverage hotel portfolios, we are going to need a lot of equity. Funds have capital and they are looking for winners and losers. They are looking for people with expertise. Some real estate might be leveraged at 40% but hotels may be even less leveraged.

All the deals done in 2005-07 have to come out of the system.”

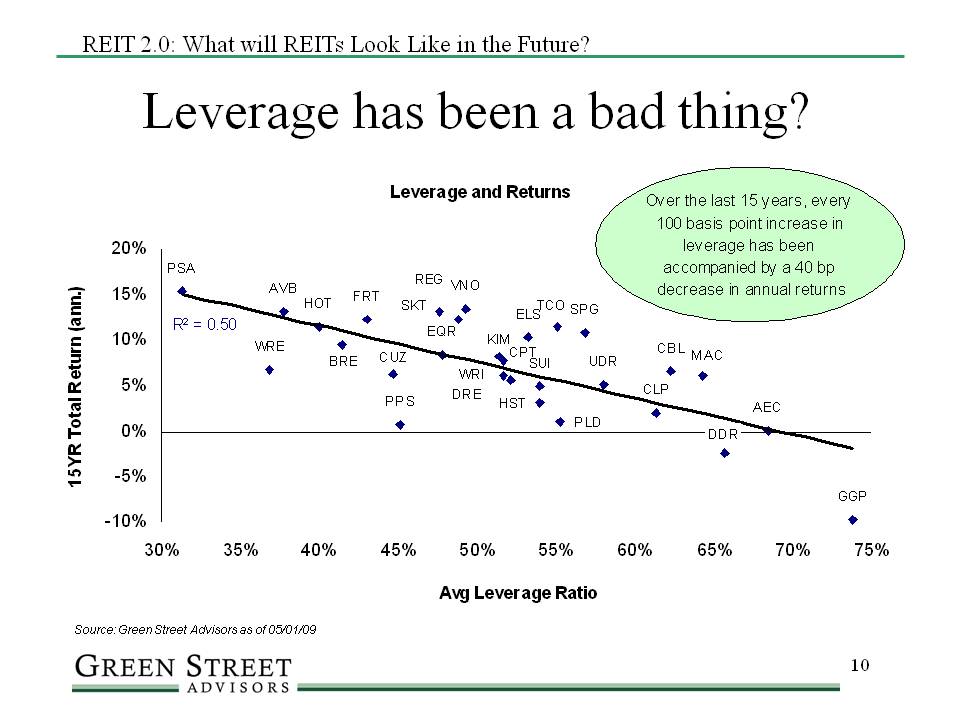

A surprising new study that leverage is deadly

Over the last 15 years, every 100 basis point increase in leverage has been accompanied by a 40 basis point decrease in annual returns

John V. Arabia, Managing Director of Green Street Advisors, is a very bright guy. I remember him as the industry leader who first figured out that with the massive equity, and vast cheap debt being controlled by the private equity guys, literally every hotel company in America was potentially up for purchase. Less than 6 months later, Blackstone bought Hilton.

Then, he figured out the correlation between airline seat capacity and hotel room demand (.3 to 1.0), and predicted the significant hit the hotel industry would take from the spiraling airline industry cutbacks.

On May 7, 2009, at Meet the Money® 2009, he gave us his latest proposition, and perhaps one of the most controversial: Over the long term, investment yield varies inversely to leverage. Yes, the unlevered investments fared best, trailed by investments with moderate leverage, and finally dogged by the more heavily leveraged investments.

Here is the important slide demonstrating the results of analysis over a complete investment cycle from the end of the credit crunch in about 1993 to the middle of the current one in 2009. John says that these credit crisis cycles tend to happen about every 17 or 18 years.

John V. Arabia CPA:

Managing Director

Green Street Advisors

(949) 640-8780

jarabia@greenstreetadvisors.com

More importantly, according to John, Institutional investors now believe the there is a direct correlation between increased leverage and decreased annual returns.

The general expectation is that moderate leverage creates higher returns.

This chart shows that companies with lower leverage outperformed those with moderate leverage, which again outperformed those without high leverage.

The cost of distress created by a capital crunch every 17 or 18 years is so great that it wipes out the benefits. As to just avoiding the last most excessive years of a cycle, John says that is a little like thinking you can time the stock market to call the top or the bottom. But even more importantly, Johns says the same conclusion would have applied if you marked performance in 2006 — before the credit crash, or if you took ten year periods in the middle.

“Over the last 15 years, every 100 basis point increase in leverage has been accompanied by a 40 basis point decrease in annual returns,” says Arabia.

The implications are profound. More importantly, according to John, Institutional investors now believe the there is a direct correlation between increased leverage and decreased annual returns. They have been speaking about this for several weeks. They will demand lower leverage. Before we saw 40-50% leverage in REITs. John says, “We firmly believe that the REIT of tomorrow will operate on 20-25% leverage.”

This means a massive re-equitization of the public equity markets. This has already begun. HOST, and LaSalle have gone to the markets already. What does that mean for the rest of us?

View John Arabia’s entire slide show from Meet the Money: “State of the Public Equity Markets – Lodging & REIT Sectors”.

What does all this mean about leverage?

For a while, the only leverage we have to worry about is resetting the levels of leverage to much lower levels. But Arabia’s provocative study suggests something that has been unheard of in most real estate circles. Most real estate investors use an unlevered return to make apples-to-apples comparisons of properties, taking out particular costs of debt or availability at a given time. Most of them would never think of an unlevered investment providing a higher yield.

Could this be a new reality for us?

In another session, I found the comment of Ambrose Fisher, Managing Director or Oaktree Capital, to reflect the more traditional view, even if done with tongue-in-cheek. Commenting on the low debt levels that are being talked about, Ambrose said, “This is America. Ultimately greed takes over . . . Leverage will go up eventually.”

This is Jim Butler, author of www.HotelLawBlog.com and hotel lawyer, signing off. We’ve done more than $87 billion of hotel transactions and have developed innovative solutions to unlock value from troubled hotel transactions. Who’s your hotel lawyer?

________________________

Our Perspective. We represent hotel lenders, owners and investors. We have helped our clients find business and legal solutions for more than $125 billion of hotel transactions, involving more than 4,700 properties all over the world. For more information, please contact Jim Butler at jbutler@jmbm.com or 310.201.3526.

Jim Butler is a founding partner of JMBM and Chairman of its Global Hospitality Group®. Jim is one of the top hospitality attorneys in the world. GOOGLE “hotel lawyer” and you will see why.

JMBM’s troubled asset team has handled more than 1,000 receiverships and many complex insolvency issues. But Jim and his team are more than “just” great hotel lawyers. They are also hospitality consultants and business advisors. For example, they have developed some unique proprietary approaches to unlock value in underwater hotels that can benefit lenders, borrowers and investors. (GOOGLE “JMBM’s SAVE program”.)

Whether it is a troubled investment or new transaction, JMBM’s Global Hospitality Group® creates legal and business solutions for hotel owners and lenders. They are deal makers. They can help find the right operator or capital provider. They know who to call and how to reach them.