Author of www.HotelLawBlog.com

22 May 2007

Hotel Lawyer reporting from Meet the Money® hotel financing conference. At the recent Meet the Money® conference on hotel financing, Mark Woodworth, Executive VP of PKF Consulting, presented the latest report from PKF Hospitality Research to a crowd of more than 450 hotel industry leaders who gathered to connect with all the top debt and equity financing sources for hotels and hotel-related projects. (For more details on the Conference or the materials from it, see “Hotel financing gateway. Meet the Money® — gateway to debt and equity financing for hotels. How to get your hotel financed.“)

Mark Woodworth’s presentation helped answer the questions on everyone’s minds: (1) Where are we in the hotel cycle? (2) What is the real threat of new supply? and (3) Where do we go from here?

His information and answers were very interesting . . .

The questions about the hotel industry that are on all our minds

(1) Where are we in the hotel cycle?

Adding to the valuable data provided by Bobby Bowers of Smith Travel Research, reported on www.HotelLawBlog.com (see “Hotel Lawyer on latest U.S. Hospitality Trends from Meet the Money® hotel financing conference“), Mark Woodworth started things off by saying that “Things are great!”

• Profits: Up 44% since 2003!

• Cap Rates: Spreads 38% below historic norm!

• Values: Prices keep going up!

But where are we in the cycle? Are we nearing the peak? Are the good times about to come to an end?

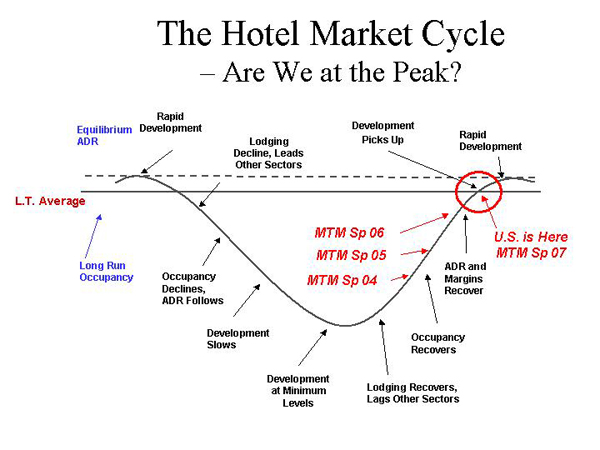

Here is Mark’s graphic demonstration of where he thinks the U.S. hotel industry is in the cycle, and also where it has been the past several Meet the Money® sessions.

Importantly, Mark notes that ADR has recovered and is still growing. (Note the long term trend lines for ADR and occupancy) Mark believes that the fundamentals are so good that although we are nearing a “peak,” we may “plateau at the peak” for some time before riding into a down cycle.

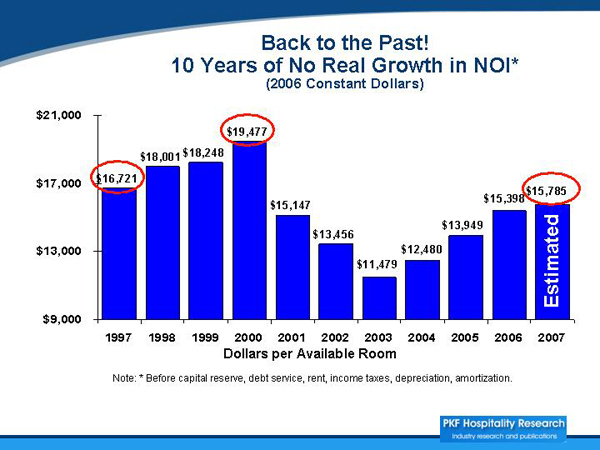

As the following chart shows, in real terms, we have not yet achieved any inflation-adjusted NOI growth from the 2000 levels. This is one factor that has dampened the economic justification for new hotel development, and consequent room supply growth during industry’s recovery over the past 5 years.

(2) What is the real threat of new supply?

But what about the threat of new supply? The hospitality industry is one that usually creates its own speed bumps by overbuilding, driving up supply faster than demand, and then watching crumbling economics. Certainly we have seen a kick up in supply, but will the results be different this time?

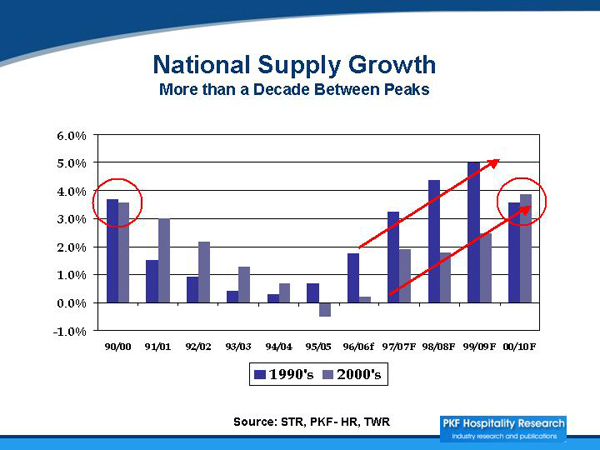

PKF research shows that there has been an incremental increase in the current construction pipeline, but Mark says, “We are nowhere near the last decade’s level of product under construction.” And here is Mark’s slide comparing the year-to-year increase in supply during the decade of the 1990s to the current decade. PKF believes that new construction will accelerate, but at levels well below what the industry saw the last time around.

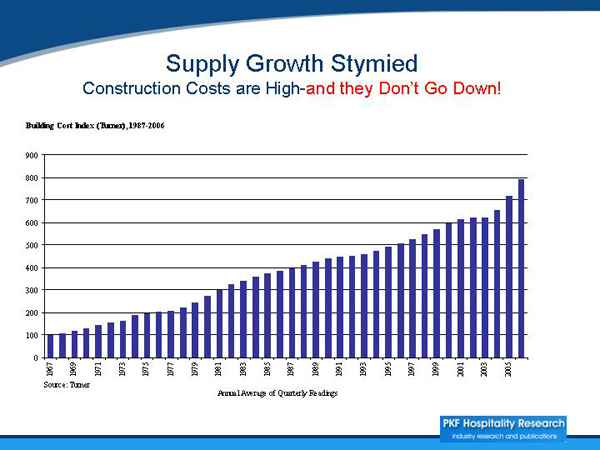

And a major reason that supply growth has dampened is the prohibitive cost of new construction, which as PKF notes, have gone up, but are unlikely to go down.

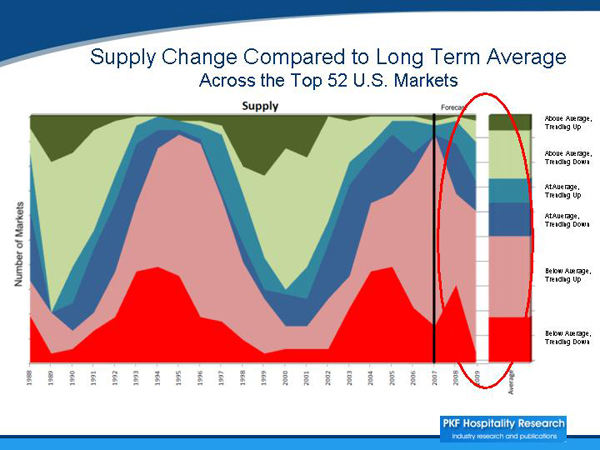

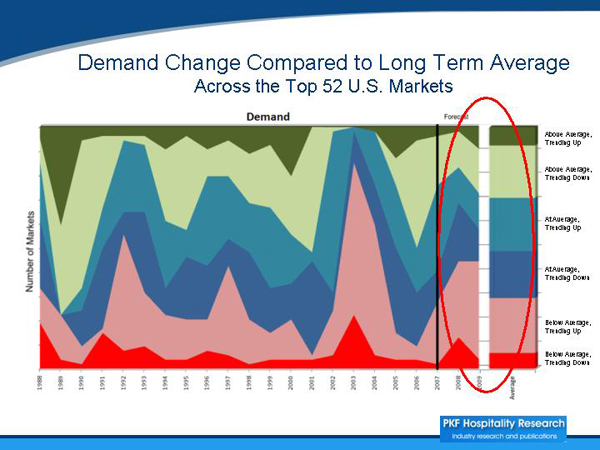

The practical, real-world consequences of all this is shown in this fascinating pair of supply and demand charts that puts supply and demand changes in perspective over the past 20 years across the top 52 U.S. markets.

(3) Where do we go from here?

Mark told the assembly at Meet the Money® that, “This is a wonderful time to be in the hotel business!” The industry’s performance the past few years has been exceptional. The strength of fundamentals continues to attract capital.

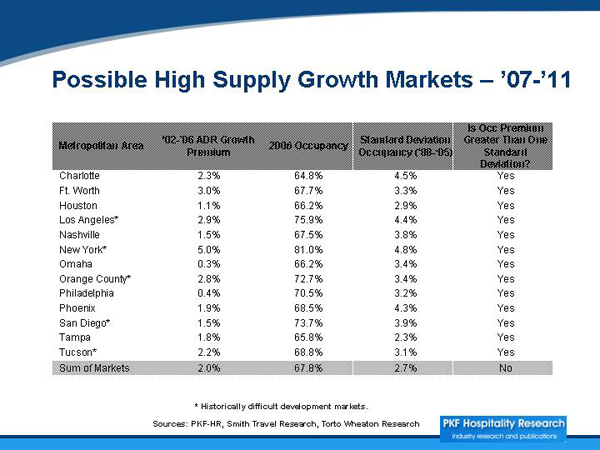

As supply ramps up, PKF sees a few high supply growth markets, which include some historically difficult markets such as Los Angeles, New York, Orange County, San Diego and Tucson.

PKF sees a slowing in the hospitality industry growth from the recent explosive few years, but compared to historic averages, things look good.

PKF’s summary of our situation and prospects.

• Strength of fundamentals continues to attract capital

• Transaction activity remains high – this condition will persist well into 2008

• Upward pressure on Cap Rates -values to level off

• Development costs remain high – no downturn in sight

• Hotel openings will begin in earnest in ’09-’10

Is the “easy” money is behind us? Yes, and here’s why:

• No more lift from cap rate compression

• Revenue growth will moderate

• Expenses keep creeping up: labor, utilities, property taxes

Even so, Mark’s summary puts it all in context. We shouldn’t forget his words when the doomsayers tell us the end is near. He said, “It remains a wonderful time to be in the hotel business!”

We couldn’t agree more.

________________________

R. Mark Woodworth, President of PKF Hospitality Research can be reached at 404.842.1150 or Mark.Woodworth@pkfc.com. For a copy of PKF’s “2007 Annual Trends” which is now available, contact Claude.Vargo@pkfc.com.

________________________

Our Perspective. We represent developers, owners and lenders. We have helped our clients as business and legal advisors on more than $125 billion of hotel transactions, involving more than 4,700 properties all over the world. For more information, please contact Jim Butler at jbutler@jmbm.com or 310.201.3526.

Jim Butler is one of the top hotel lawyers in the world. GOOGLE “hotel lawyer” or “hotel mixed-use” or “condo hotel lawyer” and you will see why.

Jim devotes 100% of his practice to hospitality, representing hotel owners, developers and lenders. Jim leads JMBM’s Global Hospitality Group® — a team of 50 seasoned professionals with more than $87 billion of hotel transactional experience, involving more than 3,900 properties located around the globe. In the last 5 years alone, Jim and his team have assisted clients with more than 90 hotel mixed-use projects, all of which have involved at least some residential, and many have also involved significant spa, restaurant, retail, office, sports, and entertainment components — frequently integrated with energizing lifestyle elements.

Jim and his team are more than “just” great hotel lawyers. They are also hospitality consultants and business advisors. They are deal makers. They can help find the right operator or capital provider. They know who to call and how to reach them. They are a major gateway of hotel finance, facilitating the flow of capital with their legal skill, hospitality industry knowledge and ability to find the right “fit” for all parts of the capital stack. Because they are part of the very fabric of the hotel industry, they are able to help clients identify key business goals, assemble the right team, strategize the approach to optimize value and then get the deal done.

Jim is frequently quoted as an expert on hotel issues by national and industry publications such as The New York Times, The Wall Street Journal, Los Angeles Times, Forbes, BusinessWeek, and Hotel Business. A frequent author and speaker, Jim’s books, articles and many expert panel presentations cover topics reflecting his practice, including hotel and hotel-mixed-use investment and development, negotiating, re-negotiating or terminating hotel management agreements, acquisition and sale of hospitality properties, hotel finance, complex joint venture and entity structure matters, workouts, as well as many operating and strategic issues.

Jim Butler is a Founding Partner of Jeffer, Mangels, Butler & Marmaro LLP and he is Chairman of the firm’s Global Hospitality Group®. If you would like to discuss any hospitality or condo hotel matters, Jim would like to hear from you. Contact him at jbutler@jmbm.com or 310.201.3526. For his views on current industry issues, visit www.HotelLawBlog.com.

The following three slides show the costs in property taxes, insurance and utilities, that continue to climb. We have seen the lift in these expenses outpace the growth of salary and wage expense. Mark cautioned that we do not see an end to this trend in the near to mid term.