20 July 2008

Hospitality Lawyer: What lies ahead for the hotel industry? On July 17, 2008, at the NABHOOD Conference in Atlanta, the experts gave us the latest update on the Hotel Industry since NYU. (See the 5-part series at www.HotelLawBlog.com analyzing the data available at June 1, 2008 at “Quips, Quotes and Insights from the 2008 NYU hotel conference.”).

Trends continue to emerge and JMBM’s hospitality lawyers have 3 hot July updates for you on the state of the industry:

1. Jan Freitag, Vice President of Smith Travel Research (jan@smithtravelresearch.com)

2. Mark Woodworth, President of PKF Hospitality Research (mark.woodworth@pkfc.com)

3. Tom Baltimore, President of RLJ Development, LLC (www.rljcompanies.com)

You can also find the Top 10 Picks from www.HotelLawBlog.com by clicking here.

Here’s Mark Woodworth’s analysis of “What Lies Ahead,” and it is very interesting . . .

U.S. Lodging Horizon 2008: What Lies Ahead?

Recession ahead . . . but how bad?

Moody’s Economy.com’s current outlook drives PKF’s forecasts, and that outlook shows a 90% probability of recession, with a 51% chance that the recession will be mild and 25% chance it will be a slow recovery. There is only a 10% chance the “mild” recession will worsen to “moderately” severe (about the same chance as a “high growth” scenario), and 4% chance of a “severe” recession.

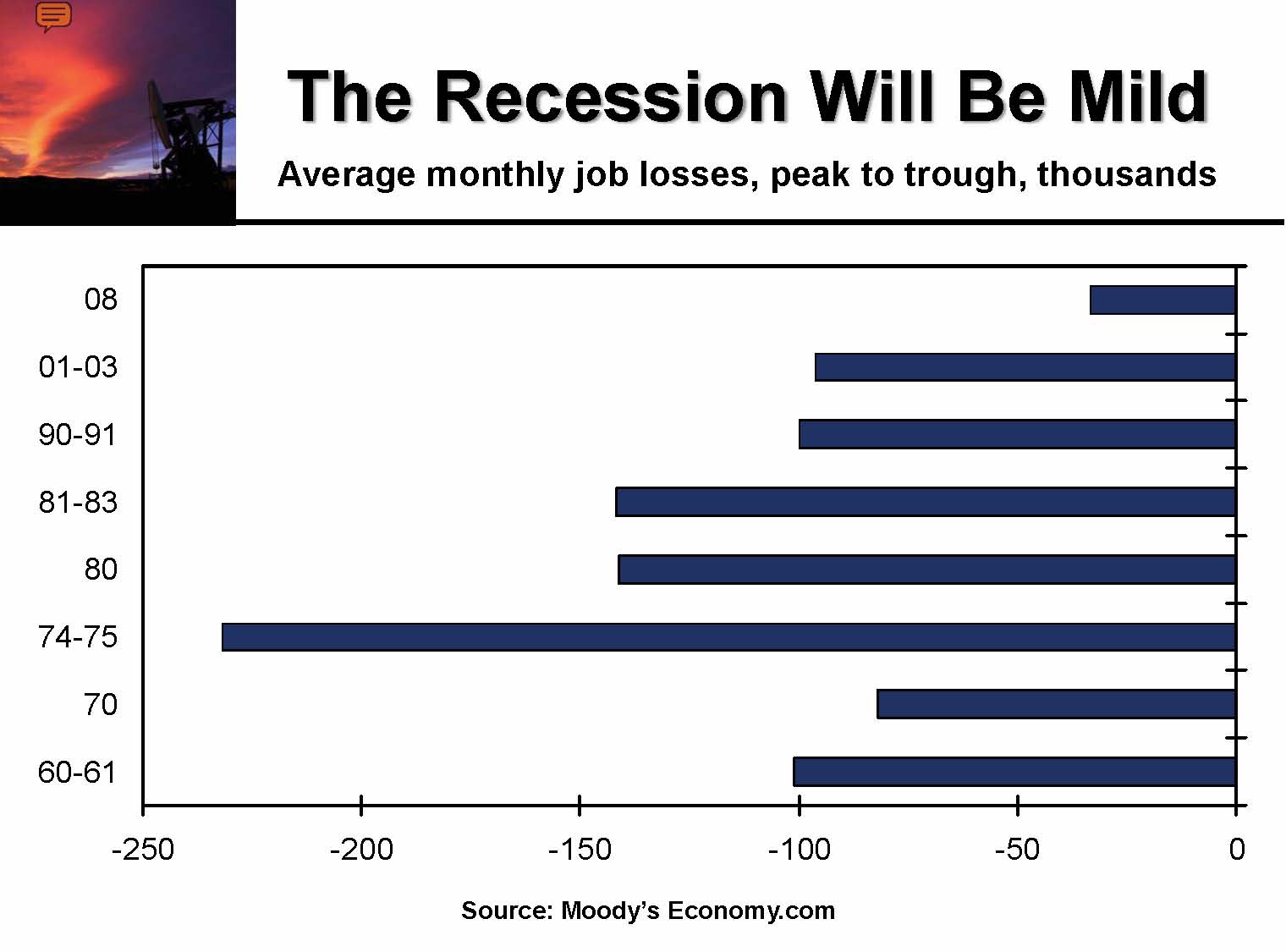

So we are likely to have a recession, but compared to the last 7 recessions, it will be quite mild, at least as measured by average monthly job losses. The following chart shows projected job losses for 2008 recession (the shortest bar in the graph at the top right), compared to past recessions identified along the left margin of the graphic.

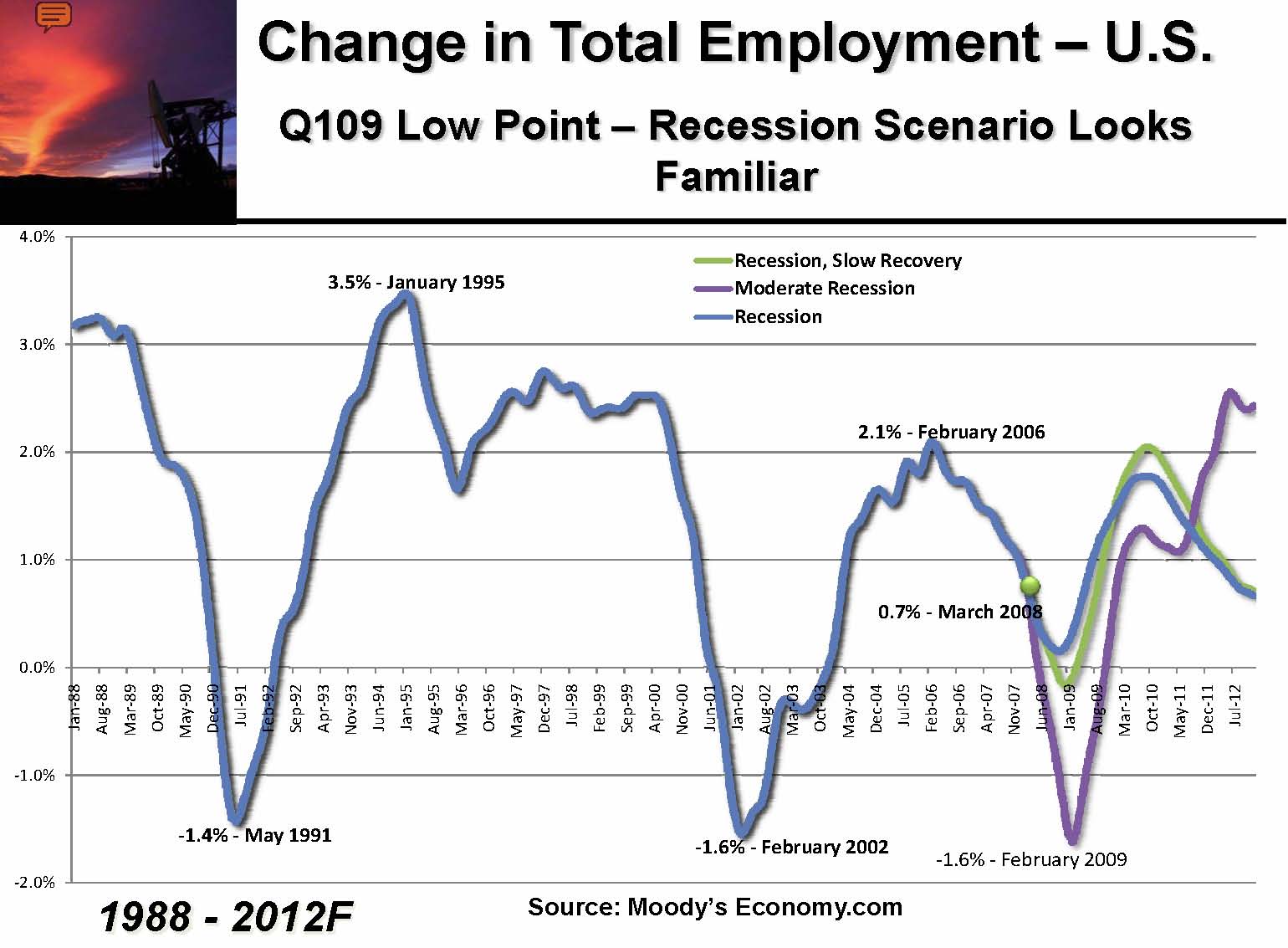

And this slide puts three possible recession scenarios (mild, moderate and slow recovery) envisioned for 2008-2012 in context of the past 20 years. In terms of total U.S. unemployment, the first quarter of 2009 is forecast to be the low point

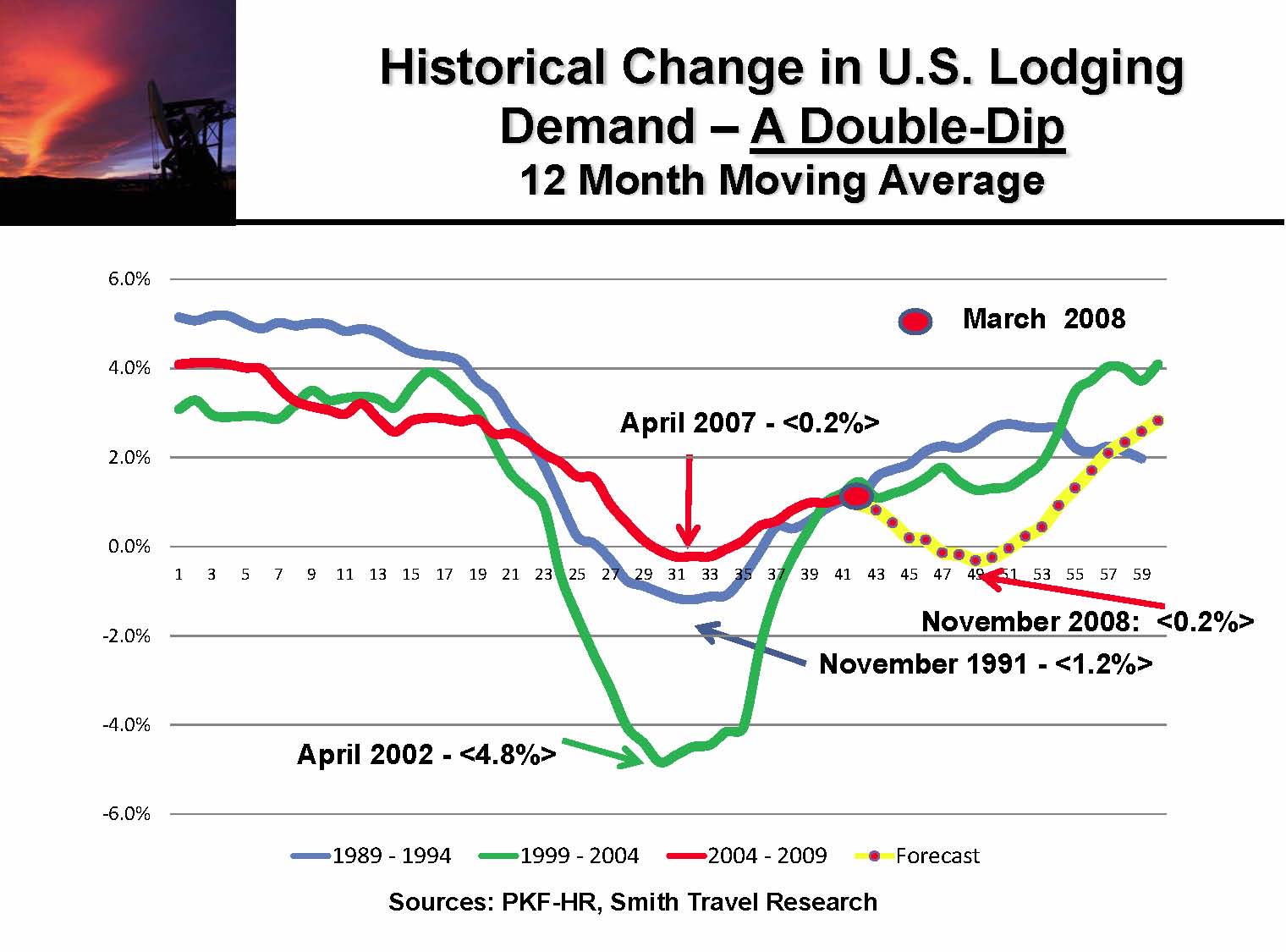

Lodging Outlook: Mild downturn, but something we haven’t seen in 20 years — a “Double Dip” in demand

If we compare the current downturn to the last two — which troughed or bottomed in terms of lodging demand in 1991 and 2002 — the current scenario is quite mild. But it is also unique, because PKF now foresees that we will have a “double dip” in demand. The first dip occurred in April 2007, and they believe the second dip will trough in November 2008.

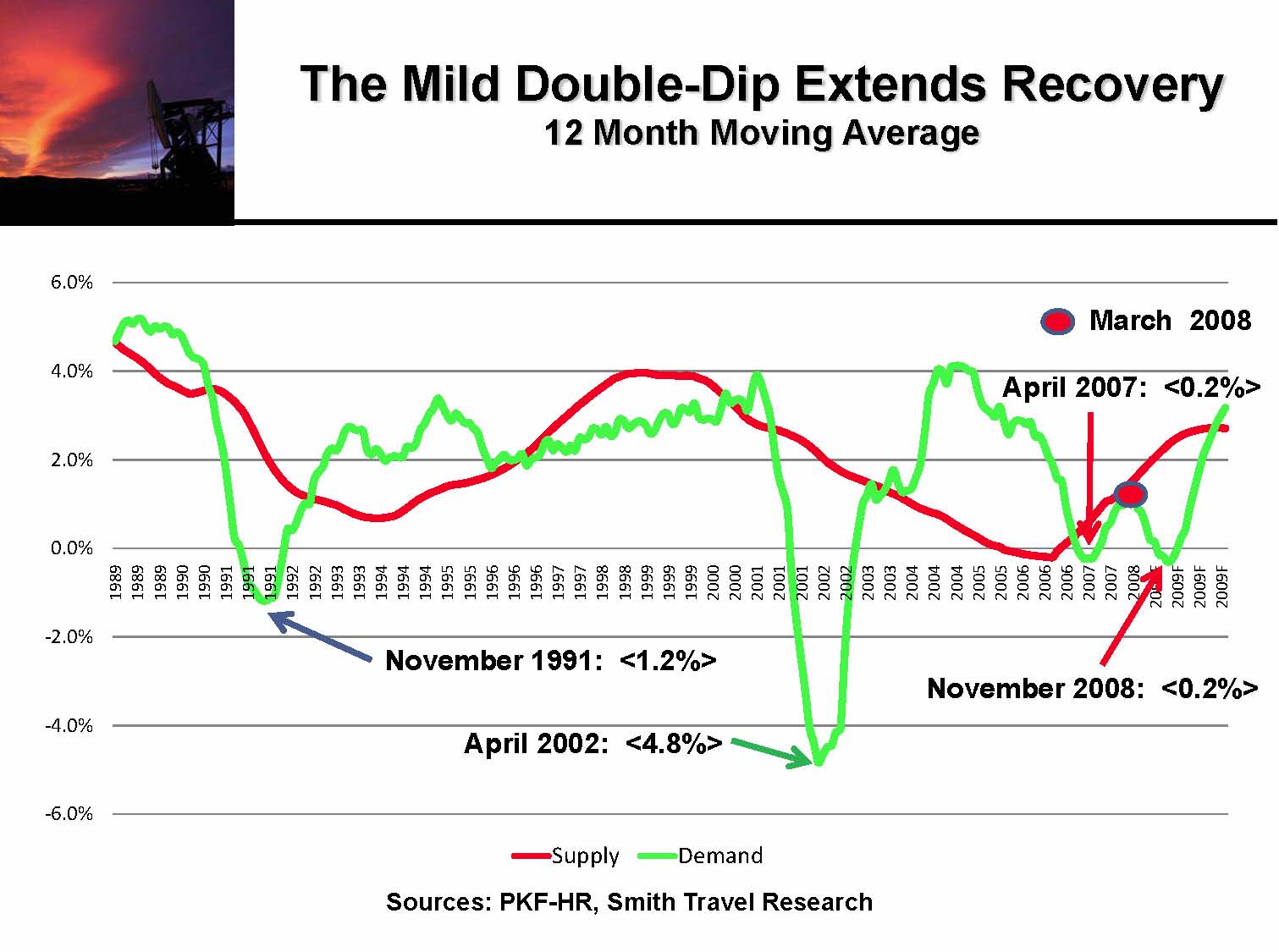

So what does the “double dip” mean for the hotel industry? It means that continuing declines in demand through November will delay or push out the recovery. The following chart shows this projection and also shows one of the critical differences distinguishing the current down turn from the last two. In both of the last two recessions, there was a significant increase in hotel room supply for some period prior to the downturns. This time around, supply growth steadily decreased from about 2000 through 2006, and even today is below the long term average.

Don’t lower your rates to make up for sagging occupancies!

PKF gives its projections on increasing ADRs by market segment (see slide show), but one important take away is becoming a mantra for owners in the current environment: Lowering rate to try to compensate for sagging occupancy is a bad strategy, and you are better off holding rate and taking a little lower occupancy.

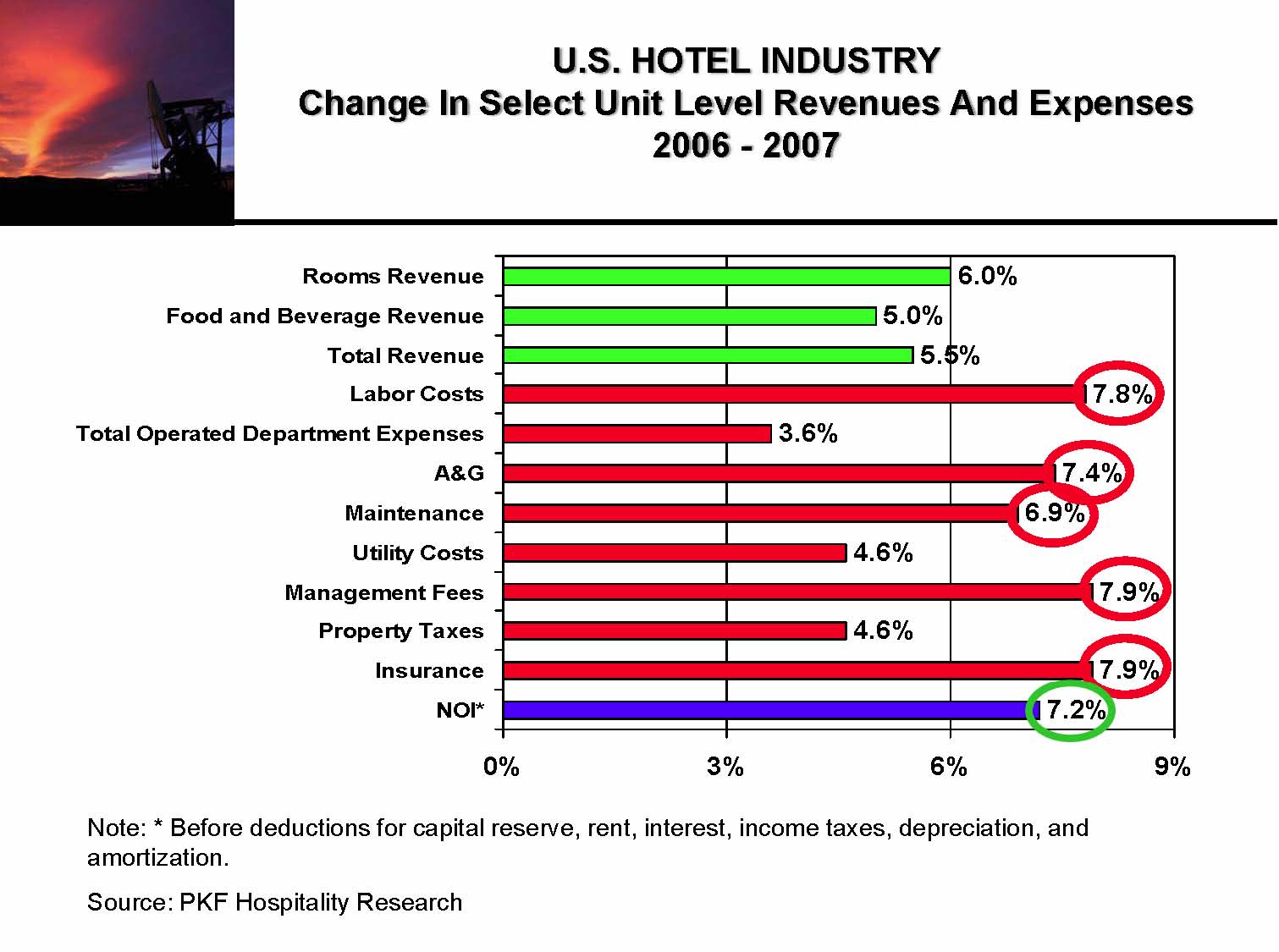

Watch out for rising expenses.

It does not take a rocket scientist to know that a lot of operating costs are going up, but this slide really highlights the dangers with a look back to changes in revenues and costs from 2006 to 2007.

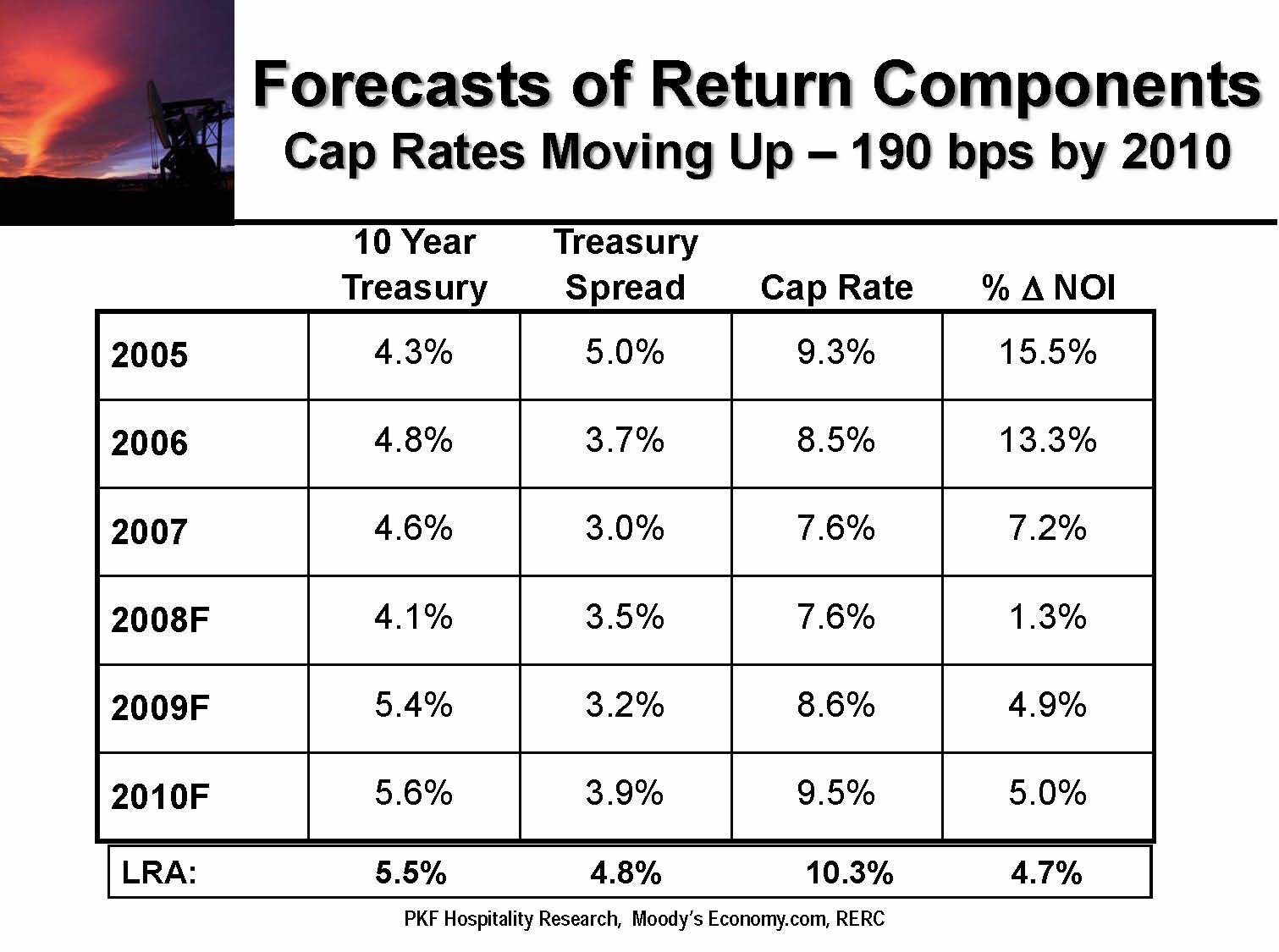

Whither cap rates?

Cap rates are an important indicator of value and value trends. (In case you missed it, one of the Top 10 Blogs is “Hotel Attorney on Hotel Cap Rates. What’s happening to hotel cap rates, values and financing?“)

Mark Woodworth is forecasting the cap rates will increase by 190 basis points between now and 2010. In fact, he predicts they will rise from 7.6% forecast for 2008 to 9.5% in 2010. In addition to cap rates, this slide also shows 10 Year Treasury rates, Treasury spreads, changes in Net Operating Income (NOI), and Long Run Averages (LRA) for each component.

Other tidbits of information from PKF

Economic expectations (for changes in employment, income, GDP and CPI) for 2007-2009 have declined significantly from October 2007 to June 2008. (slide 8)

Inbound international travel was up 10% for 2007, and is running 11.5% through April 2008, but is forecast to increase 6.0% for the entire 2008 calendar year, 4.7% for 2009 and 5.0% for 2010. The slide detail shows how certain major cities benefitted differently from this development. (slide 9)

There is a close correlation between available airline seats and lodging demand as which PKF calculates means that every 10% change in seat capacity means a 3.9% change in room demand. The correlation is shown for 20 years in the slide. (slide 10)

Inflation expectations are up 116 basis points since Q4 of 2006. Inflation lifts ADRs but hurts the overall economy and raising borrowing costs. (slide 11)

An analysis of the last 48 years, suggests that inflation rarely presents a problem for hotel profits. (slide 12)

Hotel markets will fare very differently with some having favorable RevPAR increases over CPI, and others not. See the Top 5 and Bottom 5 markets. (slide 25)

Full slide show from PKF Hospitality Research July 17, 2008

To download and see the full slide show presented by Mark Woodworth, click here.

Hospitality Lawyer’s take on things.

This current environment continues to provide great opportunity and . . .danger. Fortunes will be made . . . or lost in the coming months.

This is Jim Butler, author of www.HotelLawBlog.com and hotel lawyer, signing off. We’ve done more than $87 billion of hotel transactions and more than 100 hotel mixed-used deals in the last 5 years alone. Who’s your hotel lawyer?

________________________

Our Perspective. We represent developers, owners and lenders. We have helped our clients as business and legal advisors on more than $125 billion of hotel transactions, involving more than 4,700 properties all over the world. For more information, please contact Jim Butler at jbutler@jmbm.com or 310.201.3526.

Jim Butler is one of the top hospitality attorneys in the world. GOOGLE “hotel lawyer” or “hotel mixed-use” or “condo hotel lawyer” and you will see why.

Jim devotes 100% of his practice to hospitality, representing hotel owners, developers and lenders. Jim leads JMBM’s Global Hospitality Group® — a team of 50 seasoned professionals with more than $87 billion of hotel transactional experience, involving more than 3,900 properties located around the globe. In the last 5 years alone, Jim and his team have assisted clients with more than 100 hotel mixed-use projects — frequently integrated with energizing lifestyle elements.

Jim and his team are more than “just” great hotel lawyers. They are also hospitality consultants and business advisors. They are deal makers. They can help find the right operator or capital provider. They know who to call and how to reach them.

Contact him at jbutler@jmbm.com or 310.201.3526. For his views on current industry issues, visit www.HotelLawBlog.com.